As the world’s first, ‘whole system management’ institute, MI has a set of universal standards. We use these to rate how well organizations are performing today and the probability that they will continue to perform and grow in value. The rating process is based on a set of questions – the OM30 – and the subsequent ratings (OMRs) form our global OMINDEX.

This methodology has already been applied to some of the world’s largest corporations. Having a universal rating scale means we can compare any two or more organizations, from any sector, on a common basis.

We recently published a comparative study of the banking sector, which compares the governance, culture and human capital management of 20 large banks. In fact it was the support given in 2008, to bail out the failing banks, that made us all wake up to the true meaning of the phrase ‘too big to fail’. What the world has yet to wake up to is the fact that this same, worrying syndrome has infected other, equally important, sectors and the professions that serve them.

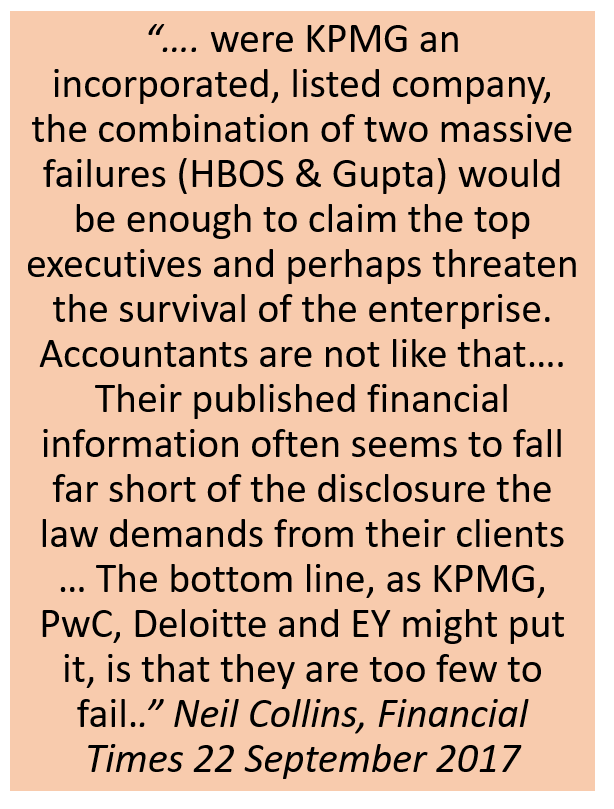

This is why MI has turned its its gaze now to the biggest accounting and auditing firms to build the Accounting & Auditing sector on OMINDEX. Our examination will first apply our analytical and diagnostic test to each of the ‘Big 4’. They are, in order of revenues ($billions), Deloitte (36.80) PWC (35.90) EY (29.60) and KPMG (24.44). The group that FT commentator, Neil Collins, refers to as the ‘too few to fail’.

As with all MI projects, we follow our evidence-based philosophy and methodology to build an insightful picture from which we can start to draw inferences and conclusions. MI’s professional protocol requires us to contact the firms that we are planning to rate, in advance, to invite them to engage with us in a process that is in their best interests. However, the first step any organization has to take, on its journey towards maturity, is to recognise and acknowledge its baseline. Immature organizations do not invite scrutiny; even when it is designed to increase their value. That is the vicious circle of immaturity and the Catch-22 that prevents modern capitalism from reinventing itself.

As with all MI projects, we follow our evidence-based philosophy and methodology to build an insightful picture from which we can start to draw inferences and conclusions. MI’s professional protocol requires us to contact the firms that we are planning to rate, in advance, to invite them to engage with us in a process that is in their best interests. However, the first step any organization has to take, on its journey towards maturity, is to recognise and acknowledge its baseline. Immature organizations do not invite scrutiny; even when it is designed to increase their value. That is the vicious circle of immaturity and the Catch-22 that prevents modern capitalism from reinventing itself.

There is already growing evidence that standards of professional integrity, governance and audit quality amongst the Big 4 have been slipping for some time. Maturity analysis reveals the potentially calamitous consequences of this behaviour. None of the offences committed by these firms can be viewed as isolated incidents. Auditing is a systemic activity critical to the healthy functioning of the whole system. Any break in the trust in the system could result in its total collapse (as already witnessed in 2008). It is Collins’ insightful analysis that helps to explains why so little, if anything, has been done by the authorities to halt this deteriorating situation.

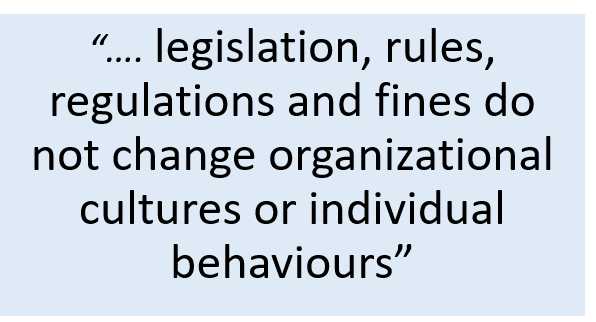

Even if governments, regulators and professional bodies had the will to act, and keep these firms and their most senior partners in line, they do not currently possess the capability to cure the deep-rooted causes of this systemic problem. Moreover, MI has already revealed a very significant lesson from the banking sector: legislation, rules, regulations and fines do not change organizational cultures or individual behaviours. Even today, the default response of the most immature banks, in the face of any new legal moves designed to exert further control, is to seek a ‘work around’.

MI deals with the real world. Our aim is to bring about lasting, positive change. This starts with a much more thorough and comprehensive auditing process, including 30 factors (OM30) that are not well integrated in organizations and do not feature in conventional accounting and auditing practice. So we are inviting any auditing firms, that acknowledge the general fall in standards, to engage directly with MI on this project.

Of course, at MI we fully recognise that change is uncomfortable and expect vested interests to resist any raising of the bar for professional standards. However, we would advise that resistance is a very risky response. Arthur Andersen’s values, before its collapse after the Enron debacle, included ‘Integrity, Respect, Passion for Excellence, One Firm, Stewardship and Personal Growth’. When Andersen ditched its values and principles, and put its partners’ profits before its societal purpose, its collapse was inevitable. The current model of ‘professional service firms’, who do not practice professionally, is unsustainable.

So we might have to witness a repeat of Andersen’s fate in one of today’s Big 4; before the others are prepared to change their ways. If this logic, in itself, is not sufficient to bring about the necessary change they should also wake up to the fact that the world around them is changing. Society is demanding that corporations declare a renewed commitment to societal purpose, better leadership, and higher ethical and professional standards. Embracing and adapting to this enlightened form of capitalism will be critical for those firms that wish to be here in the long term.

We are also looking for partners and potential sponsors for this extremely important project. So, if you would like to contact me in the first instance, in confidence, I will be more than happy to explain how we are planning to run this project and what areas we expect our final report to cover. In the meantime please see our outline plan for further information.

Paul Kearns, Chair, MI

Comments are closed